randn('seed',1);

rand('seed',1);

m=40; n=2; A = randn(m,n);

xex = [5;1];

pts = -10+20*rand(m,1);

A = [ones(m,1) pts];

b = A*xex + .5*randn(m,1);

outliers = [-9.5; 9]; outvals = [20; -15];

A = [A; ones(length(outliers),1), outliers];

b = [b; outvals];

m = size(A,1);

pts = [pts;outliers];

fprintf(1,'Computing the solution of the least-squares problem...');

xls = A\b;

fprintf(1,'Done! \n');

fprintf(1,'Computing the solution of the huber-penalized problem...');

cvx_begin quiet

variable xhub(n)

minimize(sum(huber(A*xhub-b)))

cvx_end

fprintf(1,'Done! \n');

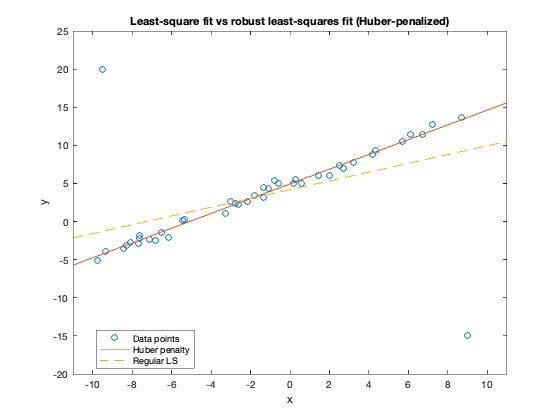

figure(1); hold off

plot(pts,b,'o', [-11; 11], [1 -11; 1 11]*xhub, '-', ...

[-11; 11], [1 -11; 1 11]*xls, '--');

axis([-11 11 -20 25])

title('Least-square fit vs robust least-squares fit (Huber-penalized)');

xlabel('x');

ylabel('y');

legend('Data points','Huber penalty','Regular LS','Location','Best');

Computing the solution of the least-squares problem...Done!

Computing the solution of the huber-penalized problem...Done!