randn('seed',0);

m=20; n=10;

A = randn(m,n);

[U,S,V] = svd(A);

S = diag(logspace(-1,1,n));

A = U(:,1:n)*S*V';

B = randn(m,n);

B = B/norm(B);

b = randn(m,1);

fprintf(1,'Computing the optimal solution for: \n');

fprintf(1,'1) the nominal problem ... ');

cvx_begin quiet

variable x_nom(n)

minimize ( norm(A*x_nom - b) )

cvx_end

fprintf(1,'Done! \n');

fprintf(1,'2) the stochastic robust approximation problem ... ');

P = (1/3)*B'*B;

cvx_begin quiet

variable x_stoch(n)

minimize ( square_pos(norm(A*x_stoch - b)) + quad_form(x_stoch,P) )

cvx_end

fprintf(1,'Done! \n');

fprintf(1,'3) the worst-case robust approximation problem ... ');

cvx_begin quiet

variable x_wc(n)

minimize ( max( norm((A-B)*x_wc - b), norm((A+B)*x_wc - b) ) )

cvx_end

fprintf(1,'Done! \n');

novals = 100;

parvals = linspace(-2,2,novals);

errvals_ls = [];

errvals_stoch = [];

errvals_wc = [];

for k=1:novals

errvals_ls = [errvals_ls, norm((A+parvals(k)*B)*x_nom - b)];

errvals_stoch = [errvals_stoch, norm((A+parvals(k)*B)*x_stoch - b)];

errvals_wc = [errvals_wc, norm((A+parvals(k)*B)*x_wc - b)];

end;

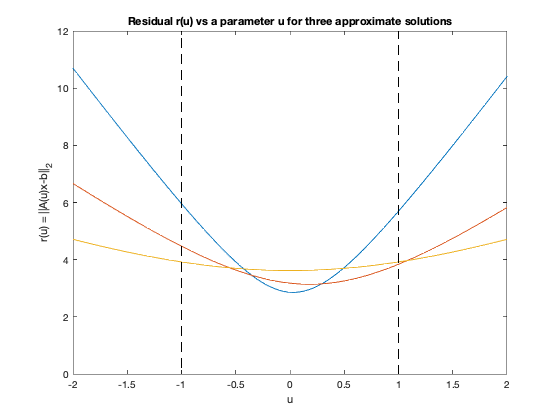

plot(parvals, errvals_ls, '-', parvals, errvals_stoch, '-', ...

parvals, errvals_wc, '-', [-1;-1], [0; 12], 'k--', ...

[1;1], [0; 12], 'k--');

xlabel('u');

ylabel('r(u) = ||A(u)x-b||_2');

title('Residual r(u) vs a parameter u for three approximate solutions');

Computing the optimal solution for:

1) the nominal problem ... Done!

2) the stochastic robust approximation problem ... Done!

3) the worst-case robust approximation problem ... Done!